Impact investing & ESG policy

- Norman Alex

- Apr 20, 2023

- 6 min read

Updated: Jun 6, 2023

The following report was written by Jérémy Genin, the Head of Global Investments and Impact Investing at Monaco Asset Management and guest of our most recent podcast. It outlines the way they believe funds and asset managers should look at ESG data to avoid green-washing and ensure the minimal carbon footprint while also maximising impact.

IMPACT INVESTING & ESG POLICY

White Paper

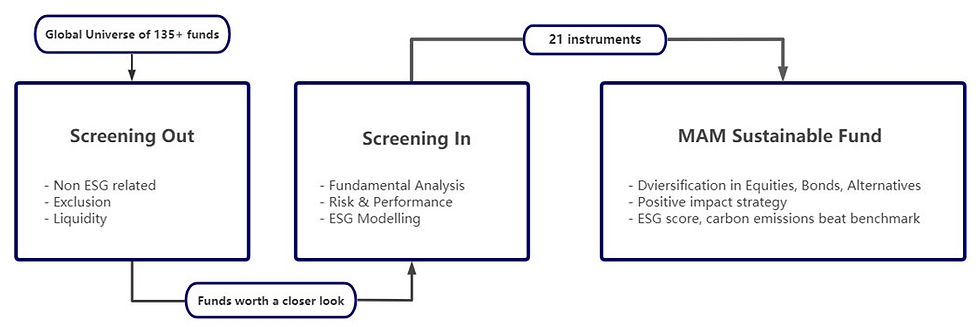

THE PORTFOLIO IMPACT INVESTING FRAMEWORK The framework aims to help construct a portfolio achieving similar risk-adjusted returns to traditional portfolios while allocating 100% of the capital to investments having tangible impacts on society. The solution is one vision, not an absolute truth. The investment objectives behind the framework are two-folds. 1. Provide an asymmetrical risk-reward profile balancing capital preservation and growth to deliver LIBOR+500/600bps returns. 2. Diversify across asset classes a portfolio composed exclusively of assets display better ESG scores and a lower carbon footprint than its respective non-ESG benchmarks. The top-down macro analysis and full cycle investing mindset provide the bedrock of the current impact investing framework with a portfolio construct similar to a “balanced” portfolio (e.g., mix of equities, bonds, and alternative investments). Under the current framework, more than 135 ESG and Impact funds globally populate the investable universe. All funds are carefully selected thanks to a rigorous due diligence process including fundamental analysis, management background review, fund composition disclosure, risk factor analyses, ESG metrics review, and performance review. The current fund universe is not solely comprised of the relatively more standard or lambda ESG funds. Instead, the framework pushes for differentiated strategies aiming to deliver solutions against climate change. These later funds are often referred to as Impact Funds. With an access to the underlying assets, the framework allows to screen out any fund with assets deemed to be in breach of the UN Global Impact principles. The remaining pool of funds represent the investable universe. When a fund becomes eligible, it undergoes a thorough due diligence and review process based on quantitative and qualitative factors. The due diligence process includes, for instance, extensive financial analyses, performance review, common checks, meetings with management teams, looking at investment cases, and assessing any potential risk factors. ESG considerations are fully integrated in the fund review process. The framework is built around ESG modelling. It relies on ESG metrics and factors to understand and assess the impact of each fund while keeping tracks of potential ESG risks in the portfolio. Thanks to a fully transparent access to fund holdings, the model has the ability to thoroughly analyse and monitor the trends of the different ESG factors it looks at. In turn, allowing it avoid greenwashed investments. Extensive investment is necessary to conduct such analysis like gaining access to third party data.

Model ESG Factors to Avoid Greenwashing

ESG MODELLING – AVOIDING GREENWASHING

The developed framework was built in the spirit of avoiding any green washing.

The below framework establishes a practical way of scoring and monitoring the ESG score of current and potential investments. It robustly and consistently applies a pre-established set of ESG criterion and metrics to rate the impact of each investments.

All of the data used and fed into the model outlined below is sourced from Bloomberg or MSCI ESG. When assessing and rating each funds or underlying, the current framework generates a comprehensive review and analysis based on the industry, ratings, rating trends, carbon emissions (scope 1 and 2) with a look-through mindset in the case of a fund (e.g., look at the holdings). Then, applying the ESG rating methodology and weight-adjusting carbon emissions, an ESG score and carbon footprint for each instrument is produced. The fitness of an investment must be unanimously be approved to be included in the portfolio.

The framework seeks to allow the construction a portfolio optimizing the balance between funds and their impact while putting in check a fund’s, company’s, or government’s ESG/Impact vision and strategy. The established framework should enable a fund to collectively create a positive environmental outcome and deliver climate solutions.

Model ESG Factors to Avoid Greenwashing

ESG POLICY

Fundamentally, the portfolio should aim to maximize its exposure to investments bringing a solution to some of the greatest ESG challenges such as climate change. While doing this, the fund should aim to lead by example on two critical metrics: (1) ensuring a better ESG and (2) a lower carbon footprint than a non-ESG equivalent portfolio.

Invest in solutions

Socially responsible investing (SRI) entails screening investments to exclude businesses conflicting with the investor’s values. SRI dates back to John Wesley, the founder of the Methodist movement who urged his followers to avoid investing in “sin stocks” generating profits through alcohol, tobacco, weapons or gambling. Common SRI exclusions in modern times include fossil fuel producers and firearms manufacturers. SRI is the simples, and often the least expensive, values-based investing approach. However, we also believe this is the least efficient use of capital. Instead, we prefer a more pro-active approach by investing in solutions not exclusions. Environmental, social, and corporate governance (ESG) investing focuses on companies making an active effort to either limit their negative societal impact or deliver benefits to society (or both). The Sustainability Accounting Standards Board (SASB) aims to standardize the ways companies report on ESG criteria to better inform investors, including determining which ESG issues companies should prioritize based on sector and industry. An example of an ESG investment might be buying shares of a technology company converting one of its data centres to use renewable energy, resulting in cost benefits and a positive effect on the environment. One step further is “impact investing” characterized by a direct connection between values-based priorities and the use of investors’ capital. These funds not only report on financial performance, but they also try to generate and quantify a positive societal impact. The portfolio we are looking to construct favours an outsized exposure to “impact funds” in the portfolio.

Achieve a better ESG score

ESG Score are designed to provide greater transparency and understanding of ESG characteristics of fund and ETF components in the fund. As the number of ESG funds proliferate, and ESG-oriented investment options and strategies are being adopted by fund managers, the process strive to provide the tools and solutions to better understand ESG risks. The goal is to optimise the portfolio’s score at all times and ensure a better result than a comparable non-ESG fund. The analysis is done at a portfolio level.

Achieve a lower carbon footprint

Institutional investors are increasingly looking to understand, measure and manage carbon risk in their portfolios. The process measures the carbon footprint of all equity investments (this process excludes fixed income investments) and calculate the carbon footprint at the portfolio level on an ongoing basis. It ensures a lower footprint than a comparable non-ESG Fund with the analysis is done at the portfolio level. This ensures leadership by example but also allows investors to go one step further and offset their portfolio carbon footprint should they wish to do so.

Engage to support the cause further

We understand that change requires engagement. It is the reason why we have long analysed and invested in “activist” funds specialised in ESG. They focus on creating positive systemic change to help build more competitive, sustainable businesses for the long run. An allocation to said strategies is recommended to optimise the fund’s Impact as long as the ESG score and carbon footprint goals are achieved.

Exclusion Policy

An exclusion is the act of barring a company’s securities from being included in a portfolio due to business activities deemed to be either unethical, harmful to society, or in breach of laws or regulations. ESG criterion are used to determine whether a firm complies with the required level of standards. If not, it would be removed from consideration under the investment framework, thus denying the company access to capital.

The current framework excludes the following sectors from the investment universe.

Arms and Weapons

Companies with more than 5% of revenues generated through the sale of weapons for the defence industry are excluded. Furthermore, the current framework bars any investment in companies producing weapons for consumer sales.

Tobacco, Alcohol, and Adult Entertainment

Tobacco has been considered and classified as unhealthy with serious long-lasting nefarious repercussions on the health of the population on top of its addictive nature. Therefore, companies with more than 5% of revenues generated from manufacturing of tobacco products such as cigarettes, cigars, and even chewing tobacco are excluded from the investable universe. Companies generating more than 5% of their revenues from adult entertainment and distilled alcohol producers are also excluded.

Controversial Behaviours Companies in violation of the United Nations’ Global Compact Principles (UNGC) and the International Labour Organization (ILO) conventions are excluded from the investable universe. It includes violations on human rights, labour, environment, and strong issues or risks surrounding corruptions. The source to identify said company is the UN Global Compact expelled list.

Sovereign Debt Environment, Social, and Governance issues are all considered as part of the framework when considering an investment in sovereign bonds. Countries not partaking to environmental conventions such as the Kyoto Protocol and the Basel Convention are excluded from the investable universe. Countries deemed to be in serious violation of human rights, political stability, peace, and religious freedom are also excluded from the investable universe. Furthermore, countries still carrying the capital punishment (e.g., death penalty) are excluded.

Excluded Controversial Countries: Afghanistan, Burundi, Central African Republic, Democratic Republic of Congo, Iran, Iraq, Libya, Mali, Myanmar, North Korea, Somalia, South Sudan, Syria, Yemen, Zimbabwe.

Policy Governance

The ESG Steering Committee (ESC) put in place as part of the framework decides on the implementation and/or changes to the exclusion policy. The ESC also has the power to decide on the additions and/or deletions from the exclusion lists.

APPENDIX – ESG MODELLING SNAPSHOTS

Investment Level

Portfolio Level

(Jeremy Genin, Head of Global Investments and Impact Investing at Monaco Asset Management).

Comments